After S&P 500 surge, five factors that could influence markets

Review the latest Weekly Headings by CIO Larry Adam.

- Equity markets have moved on, but tail risks from US-Iran conflict remain

- Sustained high energy prices would increase downside economic risks

- High bar for US earnings leaves market vulnerable to disappointing news

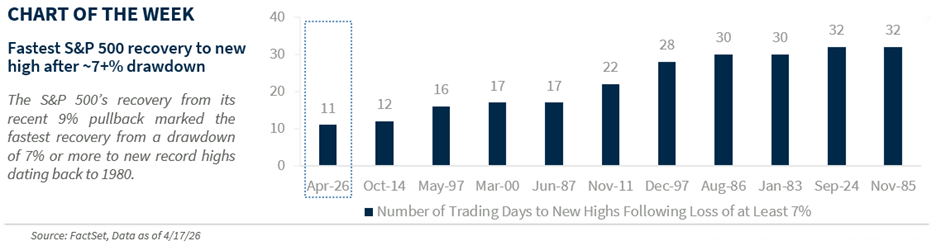

After a 9.1% drawdown, the S&P 500 surged 11% over the last 12 trading days to a new record high, breaking above the 7,000 level for the first time. To put this move into perspective: it ranks in the 99th percentile of returns since 1980 and marks the fastest recovery to new highs following a 7+% drawdown on record.

With momentum now stretched on a technical basis (e.g., 14-day relative strength index is in overbought territory at 72), investors are understandably asking whether the rally has further room to run or if expectations should be tempered. While we remain constructive longer term, we see five reasons why volatility is likely to pick up and gains may be more modest in the months ahead:

Tail risks from Iran still hang in the balance

While the two‑week ceasefire has eased near‑term tensions, equity markets appear to be pricing in a rapid resolution – and conditions on the ground suggest that may be premature. Transit through the Strait of Hormuz remains well below pre‑conflict levels, with only ~10% of normal traffic currently moving through. Oil prices have pulled back from recent highs, but at ~$80/barrel they remain well above pre‑conflict levels and are still up more than 40% year to date. Notably, the International Energy Agency warns that current prices understate the severity of the disruption given how long full normalization is likely to take. While hostilities have paused, the two sides remain far apart on key issues, including Iran’s uranium enrichment program and the full reopening of the Strait post ceasefire, leaving downside risks firmly in place. Economic damage has been contained so far, but with the conflict now entering its eighth week and US military activity ongoing, delays in reaching a durable peace agreement could trigger another setback.

Resilient but increasingly fragile economy

Thus far, the economy – particularly consumer spending – has remained resilient despite rising energy prices. That resilience has shown up in recent commentary from bank CEOs during earnings calls and is reinforced by continued strength in real‑time activity indicators such as TSA screenings, hotel occupancy and gasoline demand. That said, some early signs of strain are beginning to emerge. The University of Michigan’s preliminary consumer sentiment reading fell to a record low of 47.6 in April, while the Beige Book noted that consumers are increasingly stretched and that businesses are delaying investments amid elevated uncertainty. In addition, energy‑sensitive industries – most notably air travel – are starting to see softer future bookings. While we expect the economy and consumer spending to hold up in the near term, sustained high energy prices would materially increase downside risks.

Fed chair transition faces key hurdles

Kevin Warsh’s confirmation hearing before the Senate Banking Committee is set for April 21, but it’s unlikely he’ll be in place to lead the Fed by May 15, when Chair Jerome Powell’s term ends. Markets currently see only about a 40% chance of that happening. The main holdup is on Capitol Hill, where Senator Thom Tillis, a key swing vote on the Banking Committee, has indicated Warsh’s nomination won’t move forward while the Justice Department’s investigation into Powell remains unresolved. Adding another layer of uncertainty is Powell’s decision to stay at the Fed after his term ends, a departure from past practice that could complicate the leadership transition. From a market standpoint, Warsh would be stepping into a difficult environment, with inflation still elevated, the labor market showing signs of strain and growing political pressure to cut rates. Taken together, that uncertainty – and the market’s tendency of testing new Fed Chairs (sometimes with significant equity pullbacks) – points to higher volatility in the months ahead.

Overly optimistic earnings

Positive earnings revisions have provided important fundamental support for equities year to date. The +3.7% upward revision to 2026 earnings per share (EPS) ranks as the third‑strongest at this point in the year over the past two decades. However, emerging headwinds – including higher energy prices, supply constraints and signs of weakening global demand highlighted by luxury retailers – are likely to pressure forward estimates and contribute to higher volatility in the months ahead. This pattern echoes the early stages of the 2022 Russia–Ukraine war, when estimates initially moved higher before being revised lower as conditions evolved. Notably, first‑quarter results capture only one month of Iran‑related impacts, making forward guidance and management commentary especially important. With expectations elevated, earnings misses are likely to be punished.

Equity performance is typically weaker in mid-term election years

With attention focused on oil prices and geopolitical risks, investors may be overlooking an important backdrop: This is a mid‑term election year. Historically, mid‑term years have seen deeper intra‑year drawdowns – roughly ~20% versus an average of ~16% in a typical year going back to 1928. They have also tended to experience higher volatility, particularly mid‑year, while delivering below‑average – but still positive – returns of ~3% compared with ~7% in a typical year. This backdrop reinforces our view that further upside is likely to be modest.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.